Growth is the natural state of modern economies. But from time to time, a nation's — or the world's — economy stops growing and shrinks, anywhere from a little to a lot, before returning to growth. Economic experts call those occasional periods "recessions" and have proposed many theories about why they inevitably interrupt the natural course of economic growth.

Recessions can cause hardship for many people, as businesses fail and unemployment rises. But they also create new opportunities for business and investment.

What Is a Recession?

A recession is a period of negative economic growth characterised by falling sales and production, rising unemployment and falling real personal incomes. It is often accompanied by stock market crashes, debt defaults, foreclosures and bankruptcies. Inflation usually falls during a recession and can be negative, a condition known as deflation. Business and consumer confidence is low and there's a general feeling that times are hard.

A recession is defined as two consecutive quarters of reduced economic growth, usually accompanied by a significant rise in unemployment, decreased levels of household spending, and lower levels of business spending.

To illustrate, Australian Bureau of Statistics (ABS) records show that in the June 2020 quarter, the GDP dropped by a record 7 per cent, the second consecutive quarter of falls, with the unemployment rate peaking at 7.5 per cent in July 2020 — the highest unemployment rate in over 20 years. These statistics indicate that Australia entered recession during the second quarter of 2020 — a consequence of devastating bushfires and the Covid-19 pandemic.

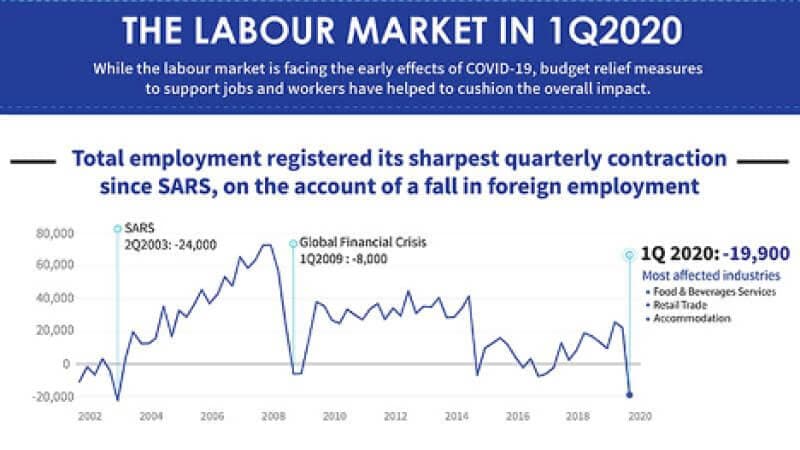

Similarly, the pandemic caused three consecutive quarters of contractions in Singapore due to the economic slowdown in major economies, global travel restrictions, supply chain disruptions, and the implementation of domestic circuit breaker measures from April to June 2020. Fortunately, these recessions were short-lived and there were signs of economic recovery in both countries by the fourth quarter.

Key Takeaways

- The definition of a recession varies from country to country, but common indicators of a recession include ongoing negative growth in real GDP, a significant increase in unemployment, decreased levels of household spending and lower levels of business spending.

- Recessions can be caused by economic shocks such as oil price spikes, financial crises, or simply by fear and uncertainty about the future. They also can be self-fulfilling prophecies, in which the actions people take to protect themselves from recession bring about the recession.

- Recessions sometimes clear out old and inefficient businesses, creating space for new, more efficient businesses to grow.

Recessions Explained

Since the start of the Industrial Revolution in the 1700s, positive economic growth has been the norm for most economies. But from time to time there are periods of slow or negative economic growth, lasting from a few months to several years. In most cases, the economy eventually bounces back to its previous growth trend, but sometimes a severe recession knocks the economy permanently onto a different growth path. The Global Financial Crisis of 2008 to 2009 was such a recession: In countries such as the U.K., the economy is still significantly smaller than it would have been had there been no recession.

Economists have proposed a variety of explanations for these periodic recessionary fluctuations. Some argue that economies are continually being hit by shocks, like a spaceship navigating an asteroid cloud. Shocks that can trigger recessions include sharp swings in oil or commodity prices, wars, disruptive new technologies, natural disasters and public health emergencies. Most shocks are small enough to cause the spaceship to deviate only briefly from its course; but occasionally an unusually big shock forces the spaceship onto an entirely different trajectory.

Other economists argue that periodic downturns are a consequence of over-investment (or "malinvestment"). In this argument, credit expands and, with money "cheap," businesses and households begin to spend in less productive ways. Debt and risk rise in the economy. Eventually, the credit bubble bursts and there is a recession in which over-indebted and inefficient businesses fail as households cut back on unnecessary spending. This clears the way for new, more efficient businesses to grow.

Some economists emphasise psychological factors as a cause of recessions. The British economist John Maynard Keynes, for example, talked about "animal spirits" influencing investment decisions. General worry about the future can lead to businesses putting expansion plans on hold and households cutting back non-essential expenditure in order to build up savings. This fall in aggregate demand causes a recession.

Monetarist economists say that recessions are the result of government policymakers' failing to regulate the money supply so as to maintain stable aggregate demand and a steady rate of economic growth. Conversely, real business cycle (RBC) theorists deny any role for monetary policy or aggregate demand in the origin of recessions. For them, recessions are always the result of real shocks to technology or productivity. For example, the COVID-19 pandemic, which featured business shutdowns, safety measures, layoffs and staff illness, was a major negative shock to productivity.

How Recessions Work

Whether it is caused by a natural disaster, a financial crisis or simply general gloom about the future, the way a recession affects the economy is always the same. The "engine" of production and consumption that drives economic growth temporarily slows down.

On the consumption side, households cut spending and increase saving (including paying down debt, which is economically equivalent to saving). This reduces demand for consumer products and services. Businesses, too, put investment plans on hold and cut back on business purchases. This reduces demand for business-to-business (B2B) products and services.

On the production side, businesses faced with falling revenue initially cut prices and reduce costs. This can involve laying off some staff, cutting working hours for others and reducing hourly wages. If cutting prices doesn't attract enough customers to sell down inventory and maintain cash flow, businesses cut production, reduce working hours and hourly wages further, and lay off more staff. Some businesses fail. If they owe money to banks or other firms, those banks and firms could potentially fail, too.

Rising unemployment and falling wages reduce real personal incomes. This sets up a negative feedback loop: As people's incomes fall, they reduce spending, forcing businesses to cut prices and production further, thus increasing unemployment and depressing wages even more.

To illustrate, from 2007-2009 the global financial crisis caused increases in unemployment, thereby decreasing production.

Unemployment Rises During A Recession

There were rises in unemployment in Singapore during the SARS, GFC and Covid-19 recessions.

Attributes of a Recession

A recession is characterised by concurrent declines in consumption, investment, production, employment and income. Inflation also usually falls in a recession, but sometimes it actually rises, for example, if a sharp rise in oil prices feeds through into persistently higher producer costs and household energy bills. There may also be improvements in some economic indicators, such as the trade balance, since falling incomes may reduce import demand while exports remain buoyant. A severe and prolonged recession becomes an economic depression.

Policymakers monitor all of these attributes to understand the likely trajectory and timespan of a recession, and to help them decide how best to support people and businesses through the hard times.

Recession Predictors and Indicators

Predicting a recession can be tricky. So much so, in fact, that there's an old joke in economic circles that goes "economists have predicted nine of the last five recessions." For example, most economists didn't predict the 2008 financial crisis and ensuing Global Financial Crisis. Metrics indicating the likelihood of a recession include GDP Growth Rates, the Consumer Price Index and Consumer Confidence.

Some recessions are preceded by stock market crashes. However, as stock market crashes don't necessarily result in widespread economic disruption, they aren't a good indicator of impending recessions. Rather, high stock market volatility can indicate growing fear of the future among investors, especially when accompanied by rising foreign currency exchange rates and falling bond yields in safe haven currencies such as the Japanese yen and U.S. dollar. CNN's Fear and Greed index gives an idea of the extent to which fear is driving investor sentiment.

Identifying exactly when the economy enters recession can also be tricky. It's often thought that the economy is in recession when there are two consecutive quarters of negative real GDP growth. But in fact, what determines whether the economy is in recession is rather more complex. The central banks use a range of economic indicators to determine whether the economy is in recession, including real GDP and its related measure, gross domestic income (GDI); real personal incomes (minus government transfers such as unemployment benefits); non-farm payroll employment; and personal consumption expenditure (PCE) inflation. Not all of these measures necessarily decline in a recession, but for most central banks to declare a recession there must be a turning point in several of them.

Recession vs. Depression

Recessions are fairly common and usually short-lived. But sometimes there is a much more severe and longer-lasting downturn — a depression.

The difference between a recession and a depression is not always easy to establish, but it is easy to misconstrue a severe recession as a depression. The accompanying chart shows some key differences economists bear in mind when deciding whether a period of falling economic activity is a recession or a depression.

Recession vs. Depression: Key Differences

| Recession | Depression |

|---|---|

| Lasts a few months or years | Lasts years or decades |

| Negative real GDP | Deeply negative real GDP (minus 10%+), usually for several years |

| Disinflation or mild deflation, but sometimes high inflation | Severe and long-lasting deflation |

| Some debt defaults and business failures | Widespread and damaging debt defaults and business failures |

| High unemployment (can be 10%+) | Extremely high and persistent unemployment (can be 30%+) |

| No significant structural changes to the economy unless deliberately introduced by government | Major structural changes to the economy caused by the effects of the depression itself |

| Economy eventually returns to previous growth trajectory | Economy remains on a lower growth trajectory than before the depression |

Types of Recessions

Recessions come in many shapes and sizes. They can be V-shaped, U-shaped, W-shaped, L-shaped, J-shaped or K-shaped. They can be deep, shallow, long or short.

- A V-shaped recession causes the least economic damage. The recession can be very deep, but it is short-lived and the economy bounces straight back to its previous growth path. The 2003 SARS recession in Singapore is an example of a V-shaped recession.

- In a U-shaped recession, there is a period of stagnation before the economy recovers, but it then bounces back to its previous growth path. The 2008-2013 recession in New Zealand was a U-shaped recession.

- A W-shaped recession is also known as a "double-dip" recession. The economy briefly recovers before falling back into recession. The second dip can be a different shape from the first: for example, the first might be a V-shaped recession, but the second a J-shape. Hong Kong experienced a multiple dip recession between 1998 and 2003 as it recovered from the Asian financial crisis.

- An L-shaped recession is the most harmful type of recession and can be very severe. It is characterised by persistently poor business investment, entrenched unemployment and slow economic growth. Charts show that the economy does not bounce back to its previous growth trajectory but remains on a lower path. The 1990-1991 recession in Japan following the bursting of its real estate bubble was an L-shaped recession: Japan has suffered persistently low growth and deflation ever since.

- In a J-shaped recession, the initial economic decline is steep and the recovery is slow and therefore takes a long time, but the economy eventually returns to its pre-recession growth trend. The Great Recession of 2008 can be considered a J-shaped recession in the U.S.

- In a K-shaped recession, part of the economy recovers quickly, while the rest takes much longer to recover. As a result, wealth and income inequality rises. The Philippines recovery from the 2020 recession is expected to be K-shaped as indicators like the gap between rich and poor, and as well the gaps between various other sectors of the economy, emerge.

Psychological Aspects of a Recession

Recessions can be caused by psychological factors such as falling consumer and business confidence, or can be self-fulfilling prophecies, where people's actions to protect themselves from the effects of recession bring it about.

Recessions also have negative psychological effects on those affected by them. Research shows that the social attributes that are characteristic of recessions, such as unemployment, falling incomes and debt distress, are significantly associated with increased rates of mental health problems, substance abuse, self-harm and suicide. The longer and deeper the recession, the more profound the impact on mental health. For example, in the Greek recession of 2008-2014, rates of depression rose from 3.3% to 12.3% and suicides increased by 40%.

Consumer Confidence

Falling consumer confidence is a principal driver of recession. When people feel gloomy or uncertain about the future, they usually cut back spending and increase saving money to protect themselves from the possibility of losing their jobs or suffering loss of income or wealth. During the 1997-1998 Asian Financial Crisis, household savings in the Philippines increased significantly from 22% in 1996 to 30% by 1998.

Behavioural Economics

Behavioural economics holds that people's behaviour cannot be fully explained by rational decision-making. The economists Robert Shiller and Richard Thaler have both shown that investors make decisions on the basis of emotion and bias as much as reason and intellect. Furthermore, even when individuals are behaving rationally, collectively their actions can be destabilising and harmful — this is sometimes known as "the madness of crowds." For example, booms and busts in financial markets can be caused by investors "following the herd" when buying (due to "fear of missing out," or FOMO) or selling (fear of losses). This creates an effect similar to someone shouting "Fire" in a crowded cinema. There may or may not actually be a fire, but everyone believes there is so they run for the exit. And in the stampede, people get crushed.

The Global Financial Crisis of 2008 was triggered by a stampede for the exit among banks and financial market investors after the failure of Lehman Brothers. But it was far from the first major recession to be triggered by a financial market panic. The Great Depression was similarly triggered by a mass sell-off by panicking investors in what became known as the Wall Street Crash. The British economist John Maynard Keynes, who lost a lot of money in that crash, ruefully concluded that "markets can stay irrational longer than you can stay solvent."

Balance Sheet Recession

The Japanese economist Richard Koo coined the term "balance sheet recession" to explain why Japan's economy didn't recover after the 1990 real estate bubble burst. Heavily indebted banks, businesses and households chose to pay down debt and shrink their balance sheets rather than investing for the future or increasing consumer spending. So the engine of production and consumption remained idling for an extended period of time, despite the Japanese government making considerable efforts to revive it. Koo observes that when the entire private sector is intent on lowering debt, the only driver of growth in the economy is government spending.

As paying down debt is economically equivalent to saving (since it increases net worth), Koo's balance sheet recession can be regarded as a version of Keynes's Paradox of Thrift. The Paradox of Thrift says that if everyone is saving, there is insufficient consumption to support current production and economic activity must necessarily fall.

Koo says that the Great Recession of 2008 triggered a balance sheet recession across much of the Western world. Households, businesses, banks and governments all deleveraged debt simultaneously, causing an extended period of very low economic growth, poor business investment and high unemployment.

Government Responses to Recessions

Governments typically respond to recessions by increasing spending and cutting taxes. To some extent, this is involuntary, because during recessions higher unemployment and under-employment raises welfare expenditure and falling incomes reduce tax revenue. These involuntary spending increases and tax reductions are known as "automatic stabilisers," since by dampening the fall in real personal incomes that a recession causes they help maintain consumer spending and thus enable the economy to recover more quickly.

Central banks usually cut interest rates in a recession to encourage borrowing. However, if inflation is high, for example, in a recession caused by a sudden sharp rise in oil prices, then the central bank might raise interest rates to bring inflation under control.

Governments also often cut the cost of credit and provide tax incentives to encourage borrowing for investment, separately from any monetary policy changes set by their central bank. For example, in 2000, the Australian government introduced a first-time home buyers grant which helped to reduce the cost of buying a house, thereby encouraging borrowing for investment.

The political and social cost of allowing very large companies that employ thousands of people to fail may lead to governments bailing them out or nationalising them to preserve jobs and communities.

Governments may also give households and businesses additional money over and above existing support schemes, or devise new schemes. The Australian Jobseeker Payments in 2020 were a fortnightly wage subsidy designed to to keep businesses trading and people employed during the COVID-19 pandemic.

In deep, long-lasting recessions or depressions, governments also enact major structural reforms to the economy to bring about robust recovery. Singapore’s 1988 Flexi-Wage Policy is an example of this.

Recession Consequences

Recessions have widespread negative effects across the entire economy, typically affecting jobs, incomes, business investment, trade, living standards, health and wellbeing. They also typically increase government debt and deficits. However, recessions usually reduce inflation, and often also reduce private sector indebtedness, whether through actual defaults or simply because people and businesses opt to pay down debts. Recessions also create opportunities for new businesses, investors with deep pockets and an appetite for risk, and nimble businesses that can easily adapt to changing economic circumstances.

Unemployment

Unemployment is typically high in a recession, though not as high as in a depression. In severe recessions, it can take a long time to return to normal. For example, global unemployment surged to over 200 million following the global financial crisis and it was estimated that 61 million fewer people were employed in 2014 than there would have been if pre-crisis employment growth rates continued.

Some recent recessions have been characterised as much by under-employment as unemployment, as people took part-time jobs rather than living on unemployment benefits and employers cut working hours instead of laying off staff. So, economists monitoring the progress of recovery now also look at full-time employment rates.

Sometimes, the labour force participation rate falls as marginal groups leave the workforce. During the COVID-19 pandemic, for example, large numbers of Hong Kong women left the workforce to care for children and eldery or sick family members. As people who are not active in the workforce are not included in unemployment statistics, a falling labour force participation rate can mean the unemployment rate appears lower than might be expected from the severity of the recession.

Business

In recessions, businesses cut back production and postpone investment decisions. The pace of recovery from the recession typically depends on how quickly businesses start investing again. Some businesses fail, particularly businesses that are badly affected by technology or productivity shocks, or which are highly indebted.

Many economists argue that business failures in a recession are necessary and desirable, because they clear out inefficient or unproductive businesses and create space for new businesses to flourish. Some economists believe the existence of "zombie" companies — those kept afloat with the help of central banks’ low interest rates but unable to generate real profits or invest for the future — contributed to the slow pace of recovery from the 2008 financial crisis.

Social Effects

Unemployment and poverty rise during recessions. In a long-lasting recession or a depression, this can increase health problems and shorten lives. Even in a short recession, those worst affected can suffer serious reduction in their wealth, which they may be unable to make up during their lifetimes.

Recessions are particularly hard on people for whom finding employment is difficult, such as older people, young people just entering the workforce and people with disabilities. When the recovery from a recession is uneven, with parts of the economy recovering more quickly than others, those "left behind" can suffer long-term unemployment and poverty. The long-lasting social effects of recessions are known as "scarring."

Benefits of a Recession

Because recessions clear out old, inefficient businesses, they can be a good time for lean, technology-savvy startups and growing businesses. And they can also be a good time for strategic acquisitions, since struggling businesses may welcome a white knight rescuer with deep pockets. Businesses can also be bought out of bankruptcy at bargain rates.

The business benefits of recessions are perhaps most obvious in the dot.com crash of 2001. Lots of technology businesses failed, but those that survived became today's tech giants — Amazon, Google and Apple, for example.

But even the recession of 2020 has business winners. Lockdowns and social distancing forced people to use streaming services instead of going to events, take vacations in their own country instead of going abroad, hold work meetings and conferences by video instead of face-to-face, and order their shopping online instead of going to the supermarket or shopping mall. Businesses that could adapt to these new ways of working and living benefited; those that couldn't adapt, lost.

Drive Business Strategy and Growth Even During a Recession

Recession is a great time to review and streamline a business, reduce costs and increase efficiency. Less profitable products and services can be cut and investment focused on those that hold the greatest promise for the future. Supply chains also need review in a recession, since it's possible some partners will fail and it's a good opportunity to renegotiate rates.

It's also worth considering whether the business can easily pivot to new growth opportunities. For example, in the COVID-19 pandemic, a company that provided sound and light technology for live events successfully switched to providing video streaming services for online events and conferences; Australian gin manufacturer, Earp Distillery, switched to producing hand sanitiser; and hundreds of restaurants started delivering high-quality meals to people's homes.

To pursue any of these strategies, businesses must have accurate financial data and strong analytical tools. NetSuite provides the needed visibility into financial and operating data that business leaders need to develop what-if scenarios and forecasts. Real-time data and reporting dashboards allow business leaders to closely monitor results and act quickly.

Conclusion

Recession is a time of hardship, but also of opportunity. By seizing the opportunity, nimble businesses and investors with an appetite for risk can not only ride out the recession but benefit from it. New business lines will deliver profits for business owners, employment to those who lost their jobs in the recession and, above all, confidence in the future.

#1 Cloud

Planning Software

Recession FAQs

What can cause a recession?

Many recessions are caused by unpredictable shocks such as natural disasters, wars, disruptive technology changes, and sudden rises in oil or commodity prices. They can also be caused by stock market crashes and banking collapses. Or they can simply arise from a general atmosphere of fear and gloom.

How long do recessions last?

Recessions can last from a few months to several years.

Can you predict a recession?

Predicting a recession is not easy, but some economists have successfully done so. For example, Australian economist Steve Keen predicted the 2008 financial crisis and recession some years before it happened.

What are the warning signs of a recession?

Signs of an impending recession can include an inverted bond yield curve, increased stock market volatility, slowing rate of bank lending, falling inflation, falling real GDP, rising unemployment, sharply falling retail sales, and falling business and consumer confidence.